2023 State Tax Law Changes

Most States enacted legislation in 2023 or have tax provisions that go into effect in 2023 due to legislation passed in previous years.

2024 Tax Inflation Adjustments

The IRS announced their annual inflation adjustments for over 60 tax provisions in tax year 2024, including increases in the standard deduction and maximum EITC.

Latest Requirements for States with Their Own Earned Income Tax Credit and Child Tax Credit

Thirty states and the District of Columbia have enacted their own version of the federal Earned Income Tax Credit (EITC). The details of each state EITC requirements are explained below.

Also, six states have enacted their own version of the federal Child Tax Credit. Of these six states, all but one also has an EITC. The details for each state are explained below.

Employee Retention Credit

Over the past few months, you may have seen information in the media about the Employee Retention Credit and the most recent news that the IRS has stopped processing any new claims for this credit due to the high incidence of questionable claims being submitted to the IRS.

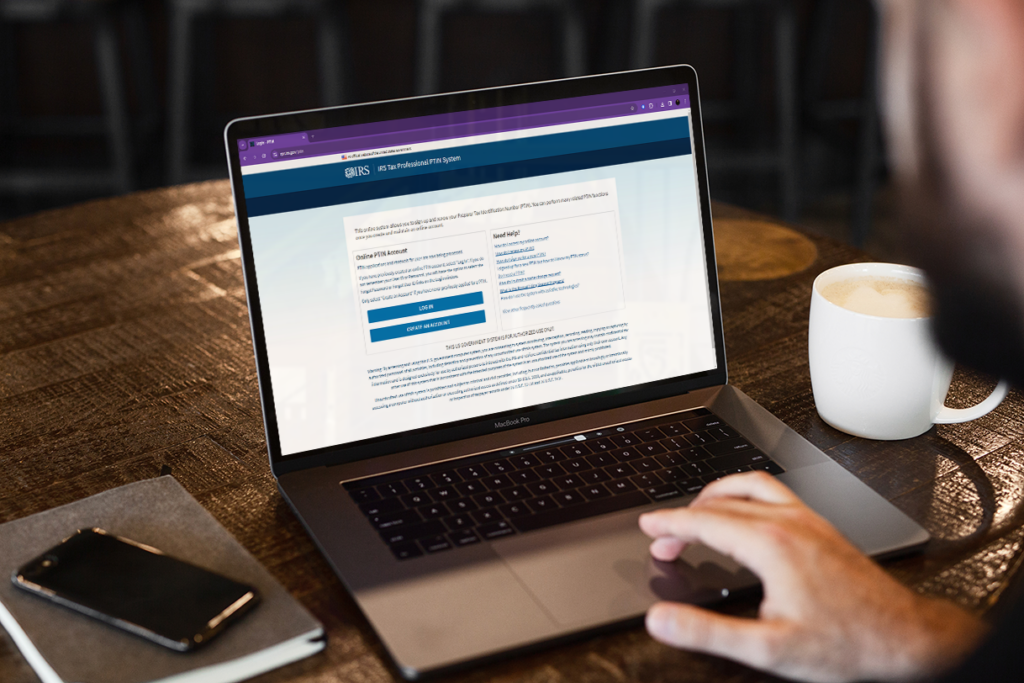

2024 PTIN Renewal is Now Open

Tax preparers may now renew their PTIN for 2024 by going to the IRS Tax Professional PTIN System page on the IRS website.

IRS Direct File Pilot Program

On October 17, 2023, the IRS announced more details on the new IRS Direct File Pilot which will be introduced during the upcoming 2024 filing season.

2023 Energy Efficient Home Improvement Credit

Energy Efficient Home Improvement Credit Included in the Inflation Reduction Act of 2022 was the Energy Efficient Home Improvement Credit (formerly known as the Nonbusiness Energy Property Credit). Is the Energy Efficient Home Improvement Credit Refundable? Taxpayers that make qualified energy-efficient improvements to their existing home in 2023 can qualify for a nonrefundable tax credit of up to $3,200 depending on what type of improvements they make to their primary residence. Business Use of Home If a taxpayer uses their home partly for business the amount of the credit is calculated as follows: What Qualifies for the Energy Efficient Home Improvement Credit? To qualify, home improvements must meet energy efficiency standards. They must be new systems and materials, not used. Some improvements have specific credit limits as follows. Heat Pumps and Biomass Stoves and Boilers For heat pumps, biomass stoves and biomass boilers the credit is 30% of their cost up to a limit of $2,000 per year. In order to qualify these items must have a thermal efficiency rating of at least 75%. The costs may include labor for installation Other Qualified Energy Efficiency Improvements and Residential Energy Expenses The credit is 30% of the cost of qualified energy efficiency improvements and residential energy expenses up to a limit of $1,200 per year. The following types of improvements or residential energy expenses (the total credit for all cannot exceed $1,200) qualify for the credit: Qualified property includes the following: The audit must identify the most significant and cost-effective energy efficiency improvements that need to be made to the residence. It must include an estimate of the energy and cost savings for each improvement. The home energy auditor must provide a written audit report to the taxpayer. How to Claim the Energy Efficient Home Improvement Credit File Form 5695, Residential Energy Credits Part II, with your tax return to claim the credit. You must claim the credit for the tax year when the property is installed, not merely purchased. For more information see the following: CrossLink Professional Tax Solutions CrossLink is the industry’s leading professional tax software solution for high-volume tax businesses. Built based on the needs of busy tax offices and mobile tax preparers that specialize in providing their taxpayer clients with fast and accurate tax returns, CrossLink has been a trusted software solution since 1989. CrossLink’s in-depth tax calculations, advanced technological features, and paperless solutions allow you to prepare the most complicated tax returns with confidence and ease while providing your customers an unparalleled experience.

2023 Used and Commercial Clean Vehicle Credits

Used and Commercial Clean Vehicle Credits The Inflation Reduction Act included two new credits for clean vehicles. They are the Credit for Previously Owned Clean Vehicles and the Commercial Clean Vehicle Credits. Both credits go into effect in 2023 and are available through 2032. Here are the details for each of these two credits: Used Clean Vehicle Credit A taxpayer who purchases an eligible used clean vehicle in 2023 may be eligible for the new nonrefundable Credit for Previously Owned Clean Vehicles. The credit is 30% of the vehicle’s purchase price or $4,000 whichever is less. Other details for this credit: For more details see the following pages on the IRS website: Commercial Clean Vehicle Credit A taxpayer who purchases a qualified commercial clean vehicle may be able to claim the new nonrefundable Commercial Clean Vehicle Credit. The credit is calculated as the lesser of: The maximum credit that may be taken on a qualifying vehicle is: Or Other details for this credit: For more details see the following pages on the IRS website: CrossLink Professional Tax Solutions CrossLink is the industry’s leading professional tax software solution for high-volume tax businesses. Built based on the needs of busy tax offices and mobile tax preparers that specialize in providing their taxpayer clients with fast and accurate tax returns, CrossLink has been a trusted software solution since 1989. CrossLink’s in-depth tax calculations, advanced technological features, and paperless solutions allow you to prepare the most complicated tax returns with confidence and ease while providing your customers an unparalleled experience.

2023 Residential Clean Energy Credit

The Inflation Reduction Act of 2022 extended and increased the Residential Energy Credit and renamed it the Residential Clean Energy Credit.

2023 IRS Security Summit

This year’s Security Summit tax professional summer campaign is emphasizing the following series of simple actions that they can take to better protect their clients and themselves from sensitive data theft.